Intel Announces Record Quarterly Revenue And Full-Year Revenue For Q4'2016

by Brett Howse on January 26, 2017 10:00 PM EST- Posted in

- CPUs

- Intel

- Financial Results

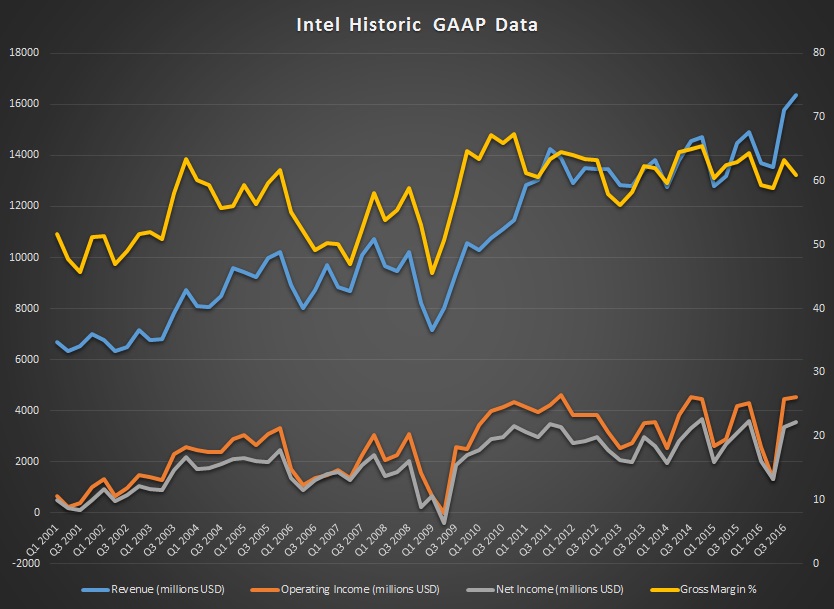

This afternoon, Intel announced their quarterly earnings for the fourth quarter of their 2016 fiscal year. Intel set a new record for revenue for this quarter, coming in at $16.4 billion. This is up 10% from a year ago. For the year, Intel brought in $59.4 billion, up 7% from their 2015 results. Intel’s gross margin fell 1.7 points to 60.9%, and they had an operating income of $12.9 billion, which is down 8% from a year ago. Net income was down 10% to $10.3 billion, and earnings per share fell 9% to $2.12.

Intel also reports Non-GAAP results, which exclude several expenditures, such as acquisition-related adjustments, write-downs, and the like. On a Non-GAAP basis, Intel had a gross margin of 63.1%, down 1.7 points, an operating income up 11% to $4.9 billion, and a net income up 4% to $3.9 billion. Non-GAAP earnings per share were up 4% to $0.79.

| Intel Q4 2016 Financial Results (GAAP) | |||||

| Q4'2016 | Q3'2016 | Q4'2015 | |||

| Revenue | $16.4B | $15.8B | $14.9B | ||

| Operating Income | $4.5B | $4.5B | $4.3B | ||

| Net Income | $3.6B | $3.4B | $3.6B | ||

| Gross Margin | 60.9% | 63.3% | 62.6% | ||

| Client Computing Group Revenue | $9.1B | +2.2% | +3% | ||

| Data Center Group Revenue | $4.7B | +4.4% | +3% | ||

| Internet of Things Revenue | $726M | +5.3% | +5% | ||

| Non-Volatile Memory Solutions Group | $816M | +26% | +26% | ||

| Intel Security Group | $550M | +2.4% | +2% | ||

| Programmable Solutions Group | $420M | -9.7% | -1% | ||

| All Other Revenue | $65M | +47.7% | +10% | ||

The gross margin impact is being attributed to a few things. Warranty and IP charges increased, as did spending on factory start-ups, due to the move to 10 nm coming this year, Client Computer Group non-platform costs, and the Non-Volatile Memory Solutions Group margins. Intel very much likes to keep their margins up above 60%, and for the moment they are still there even with these extra costs.

Intel breaks the company down into several groups. The main group is the Client Computing Group, which as the name implies, provides CPUs, SoCs, and wireless and wired connectivity products destined for PCs. Although the PC market is still down, this group had revenue for the year of $32.9 billion, which is up 2%, but platform volume is down 10%. Platform selling prices were up 11%, which makes up the difference. For just the last quarter, Client Computing Group had revenues of $9.1 billion, up 4% from a year ago. Platform volumes were down 7%, offset by selling prices up 7%. Desktop platform volume was down 9%, while notebook volumes were flat. Desktop average selling price (ASP) was up 2%, and notebook ASP was up 3%. Considering the down market, Intel continues to drive revenue here. While good for them, it means prices are high, and some competition in this space might help out the consumer.

The Data Center Group also had a strong quarter, and year. For the year, they had revenue of $17.2 billion, up from $16.0 billion a year ago. For the year, Intel saw volumes up 3% and ASP up 4%. For the most recent quarter, the Data Center Group had revenues of $4.7 billion, which was up 3%. Platform volumes were down 3%, with ASP up 6%.

Intel is slowly building it’s Internet of Things group, which had revenues for the year at $2.6 billion, up from $2.3 a year ago. Revenue for this quarter was up 5% to $726 million. The Non-Volatile Memory Solutions group had revenues for the quarter of $816 million, up 26% from a year ago, and a full-year revenue of $2.58 billion, down slightly from the $2.6 billion a year ago. Programmable Solutions is new for Intel this year, with the purchase of Altera, and this segment had revenue of $420 million for this quarter, and $1.7 billion for the year. All other revenue was $65 million for the quarter, up from $59 million a year ago.

2016 was a strong year for Intel, although it was not without its challenges. Earlier this year, Intel decided to get out of the mobile SoC space completely, abandoning it’s Atom architecture for this segment. Atom does live on for low power PCs, but any of the tablets that used the Cherry Trail Atom have found themselves without a new CPU to move to. The death of Tick-Tock also had its first new entrant in Kaby Lake, although you could easily argue Devil’s Canyon was a similar situation. But they have several new exciting technologies coming to market as well, such as 3D X-Point, and of course the expected launch of their 10 nm CPUs later this year.

Looking forward to Q1 2017, Intel is forecasting a midpoint revenue range of $14.8 billion, with margin estimates at 62%.

Source: Intel Investor Relations

20 Comments

View All Comments

mdriftmeyer - Thursday, January 26, 2017 - link

Intel is a dividend only stock. Cash out and buy AMD if you have a brain.Samus - Friday, January 27, 2017 - link

Even when AMD was competitive with Intel over a decade ago, they weren't a good buy, and haven't been since. I have never met a single person who made money on AMD stock. Some people turned out well who owned ATi stock because as we all now know, they were overvalued and AMD overpaid.Of all a-list tech companies, I couldn't think of a worst buy than AMD. I hope, someday, this changes.

Haawser - Friday, January 27, 2017 - link

Worst buy ?? It was $1.79 last March, and is now $10+ Your 'worst buy' would have made people over 5 x their money had they invested at the right time. I only *wish* I'd bought some at that price.Michael Bay - Friday, January 27, 2017 - link

You`d be outright crazy buying amd a year or two ago, and not much better now. As zen hype settles, it will return to the bottom just as quickly.yannigr2 - Friday, January 27, 2017 - link

I can understand your agony. With AMD becoming competitive in the consumer and enterprise market, Nvidia eating from the Datacenter market, Qualcomm announcing multicore ARM base server SoCs and Microsoft demostrating a Windows emulator for the ARM platform, you are probably very nervous about your Intel stock valuation. Do you sleep well at nights?Michael Bay - Friday, January 27, 2017 - link

>amd becoming competitive>muh arm servers

>201X will be a year of loonix on a desktop

I thought even the most hopeless cultist would get tired of repeating this well worn mantra set, but you guys somehow always manage to surprise.

Ej24 - Tuesday, January 31, 2017 - link

Not really. AMD will never just vanish, aside from Intel they have the only other x86 license in the world. Even if they crash and struggle they'll be bought out and you can bet there will be a bidding war over the rights to x86. Even when it was down around $1.50, just buy 1000 shares, it's only $1500, not the end of the world if they get bought out at $1.30 a share. It's already so low at that point it can't go lower. After all, their Intellectual Property simply has an intrinsic value. There was far more chance to gain than to lose back when AMD was around $2. As long as Zen is a genuine competitor to Intel again and OEM's stop relegating AMD to bargain basement models they should remain competitive at $10/share. Also if Lisa Su can keep wiping the debt off the books, they'll actually start to fill their coffers again. Thats one of their biggest detriments at this time, they have very little R&D budget with so much debt. They can't even touch the R&D and Advertising machine that Nvidia has become. But she's chipping away at it steadily. As long as the fundamentals keep improving I have no reason to believe AMD won't stay at or above $10.Nagorak - Saturday, January 28, 2017 - link

AMD was priced like it was going out of business last year and it Manchester to pull through, thus the outsized gains. However this outcome was far from certain, which meant no one could really interest more than a small amount in the stock anyway. It was just too risky. Maybe some did put a substantial amount of their network in AMD, and they were handsomely rewarded, but it was pretty much a gamble and not a prudent investment decision.Nagorak - Saturday, January 28, 2017 - link

Damn auto correct...Gothmoth - Friday, January 27, 2017 - link

and you know many people who have a clue about stock.don´t kid yourself you are probably a 20 year old gamer or a IT guy that thinks he has a clue about the stock market. such people are always the loser on the stock market in the end. that´s why it exists.. somebody has to lose money.

there are plenty of people who know what they are doing.... and they even make money when AMD drops.